Navigating the maze of cross-border payments can be daunting for any software company going global. From juggling multiple currencies to accommodating varied payment options across regions, the challenges are real.

For this reason, companies selling into Brazil have grown to love Pix. Not only is it a payment method that is instantaneous and convenient, but it’s available to anyone with a bank account in Brazil and has grown to be one of the largest payment methods in the region.

In this article, we’ll break down how Pix works and show why it’s so important to accept it at checkout if you’re doing business in Brazil.

Table of Contents

- What is Pix?

- How does Pix work?

- Pix advantages and disadvantages.

- FastSpring’s Pix experience.

Looking for an online payments partner and merchant of record that facilitates Pix and other payment methods globally? Check out our latest product announcement, sign up for a demo, or check out the platform yourself.

What Is Pix?

Pix is a payment method that enables its users to send or receive payment transfers within seconds, including on non-business days. Available in Brazil, Pix is a payment method that tends to have a lower acceptance cost because it doesn’t need many intermediaries.

Unlike some other payment methods, Pix has a few specific requirements:

| Currency | All Pix transactions happen in Brazilian Real (BRL). |

| Chargebacks | Chargebacks are available through the Special Devolution Mechanism for system errors and for fraudulent transactions. More on how this works here. |

| Bank details | To collect Pix payments, users need a bank account with a participating payment service provider. |

Pix was launched to modernize transactions in Brazil by delivering a fast, affordable, and safe experience for businesses and end users. It not only promotes financial inclusion in Brazil but also drives reduced financial costs and increases security for purchasers in Brazil.

Why Is It So Important to Accept Pix?

Pix is projected to account for 40% of the total value of digital commerce in Brazil by 2026. In addition, Pix is expected to comprise 20% of all digital commerce transactions within all of Latin America by the same year. That means that businesses accepting Pix gain access to millions of transactions yearly that they otherwise would not be able to access.

How Does Pix Work?

Pix works similarly to payment methods in the EU like SEPA and other “Account to Account” (A2A) transfers across the globe, with a few minor differences. Here’s how Pix works from a merchant’s perspective:

- Enable Pix.

- Choose a Form of Payment.

- Deliver Notification.

Step 1: Enable Pix

Pix is available exclusively through service channels of financial and payment institutions in Brazil. Individuals looking to use Pix will automatically have access to Pix via their bank’s mobile application. For businesses, Pix is available through a partner institution via a redirect at the time of purchase.

Step 2: Choose a Form of Payment

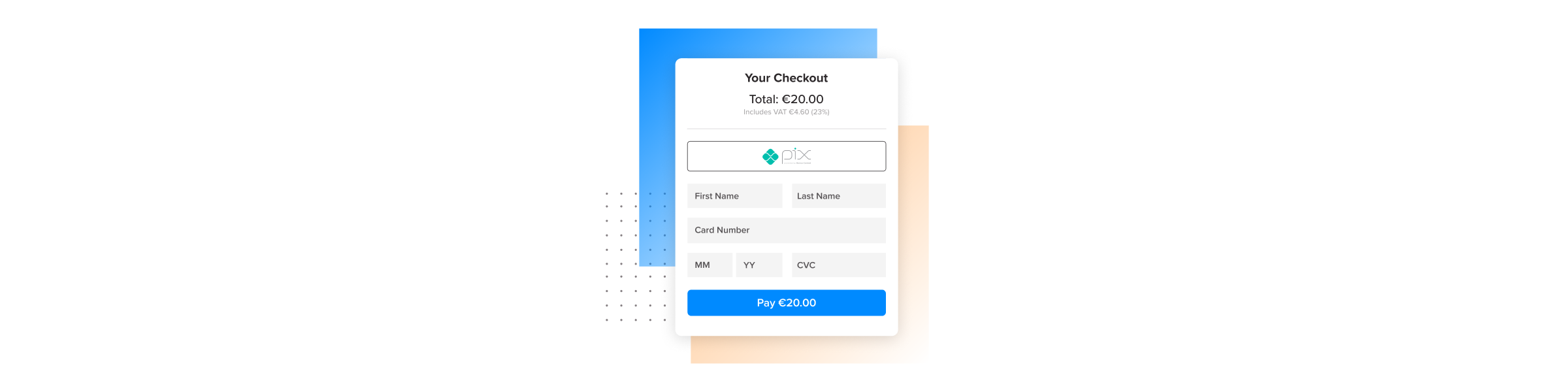

Pix offers two forms of payment collection: a Pix alias, or the scan of a QR code. The Pix alias is stored in a user’s cell phone and can be used to make a payment. Or, a QR code can be generated by the payee to start processing the payment.

Step 3: Deliver Notification

Once a Pix transaction is completed, both parties in the transaction are notified of the status of the transaction, whether it is completed or not. Then funds are immediately transferred at the end of each transaction. The confirmation gives both parties the certainty that payment and funds were received or the knowledge that it didn’t go through.

Pix Advantages and Disadvantages

Advantages

Pix has several advantages for companies:

- One stop solution for the unbanked: Pix reduces the reliance on complex identification processes. Transactions can be initiated using simpler unique identifiers such as CPF ( “Cadastro de Pessoas Físicas” which translates to “Individual Taxpayer Registry” ), which makes it easier for the unbanked population to engage in digital transactions.

- Available to all: Pix is designed to be interoperable across different banks and financial institutions across the region, which in turn avoids expensive cross border payments. This fosters a more connected financial ecosystem.

- Availability and instant payment settlements: Pix operates 24/7, allowing users to make transactions at any time — offering increased flexibility for your customers.

- Builds trust and security: Pix incorporates advanced security measures, providing a more secure environment for digital transactions and reducing the risk associated with other payment methods.

Disadvantages

Pix is not a good option for:

- Transactions outside of Brazil: As a payment method that only operates within Brazil, businesses that don’t have a presence in the country will not be able to accept payments using Pix.

- Large-scale B2B transactions: Per limits enforced by Brazilian banks, any business transacting with more than BRL 100,000 (about $10,000 USD) will be unable to use Pix to facilitate the transaction. As such they would need to seek out other options for payment.

- Recurring transactions: Users who are selling automatically recurring products are unable to use Pix to facilitate these transactions. The Central Bank of Brazil plans support in late 2024, but until then, a user would need a different payment option.

Read our documentation to learn how Pix works with FastSpring.

FastSpring’s Pix Experience

If you’re interested in offering Pix to your Brazilian customers, you can streamline the payment process by signing up with FastSpring.

Our platform automatically enables Pix for any users offering Brazilian Real (BRL) in their contextual store. Then we handle all of the steps to process your buyer’s order, so you don’t need to do anything except enable BRL as a currency for your products.

Here’s what that looks like from your buyer’s perspective:

- The customer selects Pix as their payment method.

- FastSpring asks for required personal details. If FastSpring already has the customer’s details, FastSpring creates a session without asking for the details.

- FastSpring redirects the customer to the partner’s Pix page.

- On the partner’s page, the customer provides their CPF (Cadastro de Pessoas Físicas) number, which is required for Brazilian transaction regulation.

- Once the customer confirms their details, the partner generates a QR code.

- The customer has 24 hours to scan the code and complete the transaction. During this time, the transaction status is “Pending payment”.

- If the transaction isn’t completed within 24 hours, FastSpring automatically cancels the transaction.

- Once the customer successfully completes the payment process, FastSpring displays an order confirmation.

We’re constantly optimizing our system to add payment support for more countries and to provide a smoother Pix payment experience. Let us take on your global payment needs — sign up for free today!